The Listing agent tells me the person handling the trust does not know anything about this property since they have been rented to the same families for the last ten years.

He could have her fill out disclosures with all “unknown” or can she do an “Exempt” TDS, he is asking me.

If the property is held in a trust and the trustees didn’t occupy the premises or own property outside of the trust in the last year, then the seller can use the exempt seller disclosure.

If any trustee did in fact reside at the property or owned it outside of the trust in the last year, then they are required to do a TDS.

“Unknown” should be marked as a no. A disclosure asks whether it is known, yes or no. If the seller doesn’t know then the “no” box should be checked.

Offer was contingent on inspection and we are not going till Monday morning because just today one of the families provided negative COVID results after having contracted it, if we see problems with the properties we can still cancel, correct? Yes, you can cancel until you remove the inspection contingency in writing.

Also, buyer will be flipping them, my question is with such long tenancies, is there anything we need to do besides giving them 60 days notice, and can we do it 3 days after COE?

We already wrote that number on the tenant transfer form. Yes, as long as your 60 day notice is compliant with the moratorium and give a valid reason (extensive remodel in your case). The landlord (buyer) will likely need to either pay tenant relocation or a rent waiver.

Here is the reason cited from civil code 1946.2: (D) (i) Intent to demolish or to substantially remodel the residential real property.

If an owner issues a notice to terminate a tenancy for no-fault just cause, the owner shall notify the tenant of the tenant’s right to relocation assistance or rent waiver pursuant to this section. If the owner elects to waive the rent for the final month of the tenancy as provided in subparagraph (B) of paragraph (1), the notice shall state the amount of rent waived and that no rent is due for the final month of the tenancy.

Is there a problem with me helping my buyer do that after we close? Once you close escrow, your role and duties as a real estate agent ends. Any help you do would be on a personal level. You have to be very careful to not act on the client’s behalf, especially when it comes to property management or the lease termination.

California Real Estate Seller Disclosure Timeline

In some cases, HOA document orders exceed buyer contingency periods. Below is a quick summary of the implications as they relate to seller disclosures.

*This is based on default California residential purchase agreement timelines.

The seller has 3 days from acceptance to request (order) HOA docs (This is usually done by escrow).

The seller has 7 days from acceptance to deliver all disclosures to the buyer.

The buyer has a 17-day investigation period.

OR

The buyer has 5 days from receipt of any outstanding seller disclosures listed in RPA Para. 14A

Whichever date is later – to remove all contingencies.

The purchase agreement is contingent upon HOA disclosures.

Buyer’s approval of CI (HOA) Disclosures is a contingency of this agreement…Para. 10.F.3.viii.

What happens when HOA docs have been ordered but take too long to arrive?

If all the other seller disclosures (outlined in Para. 14.A) have been delivered to the buyer, then the seller can still request a contingency removal form (CR) that can request any or all other contingencies be removed except for the HOA disclosures.

This extracts the HOA disclosure from the other seller disclosures so that the seller can duly enforce contingency removal for everything else.

Questions? email info@balboateam.com

Should a buyer ask for a price reduction or request a seller credit (concession)?

When a buyer finds out a home needs needs repairs, the buyer can:

- Ask the seller to do the repairs.

- Ask for a seller credit.

- Ask for a sales price reduction.

If the seller won’t do repairs, but is willing to compensate the buyer, then the buyer must decide whether to request the credit or price reduction. What’s the difference?

- A seller credit or concession is deducted from the seller’s side of escrow’s balance sheet and credited to buyer’s side. The seller credit directly reduces the total amount due to purchase the home.

- A sales price reduction is as simple as reducing the purchase price, yet has a negligible effect on the amount of money the buyer must bring to closing to purchase the home.

The only time a sales price reduction makes sense is if you are a cash buyer.

The reason is that a reduction of the sales price for the cash buyer is realized instantly at close of escrow. The amount of the reduction is directly deducted from the amount the buyer has to bring to closing in order to purchase the home.

This is not the case with financing buyers.

Now, I know the counter-augment. A reduction of the sales price saves the buyer on property taxes. This is true, but doesn’t even close to justifying choosing a price reduction over credit.

Let’s look at the math. Let’s say the buyer can choose between a sales price reduction or seller credit of $7,000. The price reduction of $7,000 will save the buyer ~$73 annually. If we divide the $7000 by the annual savings of $73 then we see it takes a whopping 96 years before the first year of tax savings is realized. But, hey, on year 97 you will save $73!

Let me be clear, cash and finance buyers are worlds apart in terms of their cost to acquire a property. Finance buyers are borrowing massive sums of money. It’s just very common so we are desensitized to it. The reason that finance borrowers are taking on such a massive debt is because they likely have no more than 1/5th price of the cost of the home in cash that can be used as down payment. Only 1/28th of the price of the home in cash for FHA buyers. What do these numbers mean? It means that every penny of money that can be immediately realized by the buyer is precious.

So, if a buyer can get a credit from their agent or the seller then it has tremendous financial impact. That $7000 credit from the seller instantly reduces the amount the buyer has to bring to closing. That’s $7000 more the stays in the buyer’s pocket. A finance buyer is in no position to apply it to the purchase price.

There is a missing piece – mortgage savings. If there is a reduction of the sales price then it proportionally will reduce the loan amount of the buyer. If the buyer is getting a loan for 80% of the sales price, then the loan amount should drop 80% of the credit, In this case 80% of $7,000 is $5,600. That might save the buyer $25 a month or $300 a year. Let’s say the buyer can save $370 a year on mortgage and property taxes from the $7,000 sales price reduction. It will still take the buyer 19 years to breakeven. This means that it won’t be until year 20 of home ownership that the buyer sees annual savings of $370. By then, inflation and mortgage interest have buried the abstract price reduction. Meanwhile, a $7000 credit that is as good as cash would have had a powerful impact right at closing.

The answer is simple for a finance buyer – choose the credit.

If you are interested in 100% commission real estate then please CLICK HERE for more information.

What is The Earnest Money Deposit?

Also, called the “EMD,” this is a good-faith deposit the buyer places into escrow at the beginning of the transaction. This gesture shows the buyer’s seriousness and is also at risk of being lost if the buyer breaches contract. A typical earnest money deposit is 1% to 3% of the sales price. The EMD is not refunded but rather applied to the funds needed to close escrow. For example, if the down payment of the purchase price is $100,000 then the buyer will just need to give escrow $90,000 before closing. This is because there is already a $10,000 deposit sitting in escrow.

Can I get My Earnest Money Deposit Back?

In California, the standard residential purchase agreement has buyer contingency periods. This is a certain amount of time allocated to the buyer to perform inspections or gets a loan. For example, you have 17 days from acceptance to do property inspections. If you decide the property requires too much work then you can cancel in that timeframe and are entitled to a refund of your earnest money deposit. Basically, a good rule of thumb is that if you cancel within any contingency period, your earnest money deposit is refundable.

What Happens If I Cancel After Contingency Periods?

Let’s continue our example where you’re a buyer. Now imagine all your contingencies run out on day 21. Then on day 22 you decide to cancel. Is your earnest money refundable? Maybe, I will explain. The standard in California is that the buyer must remove contingencies in writing or else they stay in effect. So, even if your longest contingecy period expires on day 21 after acceptance, it will continue indefinitely until you send the seller a written removal of contingencies. This means that as long as you didn’t remove your contingencies, your earnest money deposit is refundable.

What If I Remove Contingencies and Cancel?

Once you remove your contingencies it is assumed that your deposit is non-refundable. If you try to back out, the seller will likely ask you to surrender your deposit. If you refuse, the seller can make a claim or even take you to court to get an order for escrow to release the deposit as “liquidated damages.” The contract has a section that states the seller can keep the deposit up to 3% of the sales price as penalty for the buyer’s breach. Now, this doesn’t happen that often. Usually the parties will negotiate a reduced fee, like the seller might get half the earnest money deposit. Often the seller will not want the hassle and just refund the earnest money deposit so that they can move on with a backup buyer.

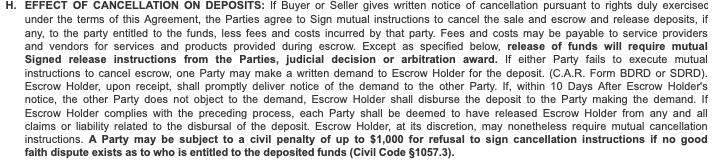

How Do I Get The Deposit Out of Escrow?

A seller that feels entitled to the deposit or a buyer that feels a refund is deserved will try to get escrow to release the deposit. Escrow cannot release the deposit without instructions signed by both the buyer and seller or a court order from one of the parties. If one party cancels due to the other party’s breach, they can demand the deposit. The purchase contract stipulates that a party can send a demand to release to escrow, and then escrow will give that demand to the other party. If the other party does not object to the demand to release deposit adfter 10 days, then escrow can release the deposit to the party that made the demand. Most parties will dispute the other party’s demand. This means the parties eather have to negotiate an agreement to release the deposit or escalate the matter to mediation/arbitration, or court.

What Happens If The Seller Refuses to Release The Buyer’s Deposit?

Neither party is allowed to hold the earnest money deposit in bad faith. This means that without a valid, reasonable claim the deposit should be released as soon as possible. Unless their is a good-faith dispute, a party must return the deposit within 30 days of receiving a written demand from the other party. Failure to return the deposit can result can result ina civil penalty up to $1000 per California Civil Code § 1057.3.

Contingenices Don’t Expire Automatically, They Must Be Removed

Contingencies stay in place until they’re removed by the buyer in a contingency removal form. So the three big buyer contingencies are the inspection period, the loan period, and then the appraisal period. Default verbiage in a CAR purchase agreement or an oorp.org purchase agreement has 17 days for the buyers inspection period, 17 days for the appraisal, and 21 days for the loan contingency. Now, sometimes I’ll get a call from a listing agent and they’ll tell me that they’re 25 days into transaction or some number of days that’s far past all the contingency periods and they’ll tell me that the buyer’s not performing or the buyers Lender is having an issue and they’re not returning calls. One of my first questions is did the buyer remove contingencies or did you as the listing agent send a notice to perform when the buyer was late on removing contingencies? Often I hear the answer’s no. For one reason or another parties forget the listing agent forget to ask or they think that once they’ve passed the contingency period that they aut

omatically expire and they come to find out that until a buyer sends that CR form that constitutes your removal form, those contingencies are in place so a buyer could drag out the contingency period for 30 days or 40 days or as long as they want because they last indefinitely. Until the seller sends a notice to perform demanding that the buyer remove their contingencies or the seller can cancel then – and the buyer of course has to respond by either cancelling or submitting their contingency removal – then those contingencies stay in place. So, it’s important to send a notice to perform if the buyers late on their contingency periods or in some transactions that are higher risk for the buyer defaulting or there’s more tension, listing agents will send a notice to perform prior to the contingency expiring because you can, you can actually send a notice to perform two days before the contingency will expire so notice perform will have a two day period let’s say it’s for a loan contingency on day 19 the listing agent can send the buyer’s agent a notice perform to remove that 21 day loan contingency and it’s a way to proactively ask that the contingencies – you’re expecting a contingency to be removed and if on the 21st day the very date of the contingency is supposed to be removed. If it’s not removed by the buyer then the seller through that notice to perform form has the option to then cancel the transaction and that allows the seller to not be stuck at the buyers whim, to not be trapped in that transaction. It allows them (seller) leverage to cancel or tell the buyer that they were going to cancel unless the buyer performs. So remember, contingencies stay in place until the buyer sends a written contingency removal form.

Interested in 100% commission real estate in California? CLICK HERE

The tutorial is not done on a CAR RPA form because CAR does not allow their forms to be used in a public forum. I obtained this form from www.OORP.org. Although it is different than than the CAR RPA, it contains the same terms that are customary to any California Real Estate transaction.

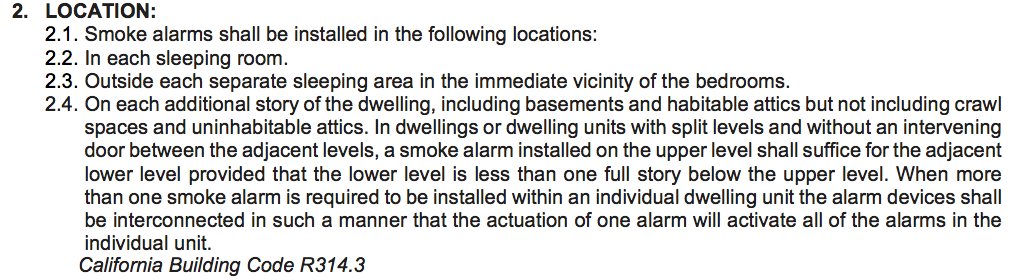

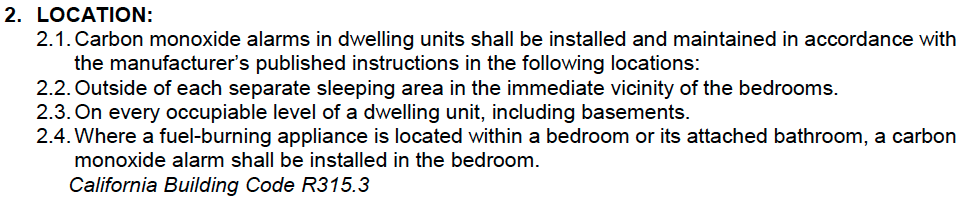

Almost all residential property sales require a smoke alarms and carbon monoxide detectors to be installed by the close of escrow.

However, there seems to be some ambiguity where they are supposed to be installed.

Here is where smoke alarms should be installed.

Here is where carbon monoxide detectors should be installed

…..

Here is where carbon monoxide dectors should be installed.

When is a seller exempt from a Transfer Disclosure Statement?

This question comes up very often. It’s required more often than you migh think.

By the way, if a Transfer Disclosure Statement (TDS) is needed then the Seller Property Questionnaire (SPQ) is needed too. State law makes it a package deal to use both forms on a transaction.

The following transfers are exempt from these disclosure requirements:

- The sale of new homes as part of a subdivision project where a public report must be delivered to the purchaser or a public report is not required. However, when such new homes are sold through a real estate broker, the broker owes the buyer a duty to disclose any material facts which affect the value, desirability and intended use of the property;

- Foreclosure sales;

- Court ordered transfers;

- Transfers by a fiduciary in the administration of a decedent’s estate, a guardianship, conservatorship, or trust except where the trustee is a former owner of the property;

- Transfers to a spouse or to a person or persons in the lineal line of consanguinity;

- Transfers resulting from a judgment of dissolution of marriage, or of legal separation, or from a property settlement agreement incidental to such a judgment;

- Transfers from one co-owner to another;

- Transfers by the State Controller for unclaimed property;

- Transfers resulting from failure to pay taxes; and

- Transfers to or from any governmental entity.(CAL. CIV. §§ 1102, 1102.2, 1102.3)

Social Media